The Open Web's Real Problem Is Not Just Google

A federal judge just ruled Google is a monopolist. That is the right verdict for the wrong era.

Washington just spent two years arguing about who controls the pipes of the open web. The pipes are already rusting. That is the story nobody is telling.

In April 2025, Judge Leonie Brinkema ruled that Google had built an illegal monopoly in the ad tech market. She declared that Google controlled the buyer, the auction, and the seller at the same time and used that control to tilt every auction in its favor. It was a significant ruling and a long time coming. The DOJ is now pushing for Google to sell off AdX, its ad exchange. Google wants behavioral rules instead. The industry is waiting on the remedies decision.

Here is the thing though. Whether the DOJ wins or loses, whether AdX gets sold or regulated, the open web that GAM and AdX were built to monetize is disappearing. Not slowly. Right now. And the thing killing it is not Google's ad tech stack. It is the proliferation of agents and chatbots.

WHAT GOOGLE ACTUALLY DID AND WHY IT MATTERS LESS THAN YOU THINK

Going back to the case itself because you need to understand what was actually found before you can understand why it is the wrong fight.

Google built three things that sit on top of each other. Google Ad Manager, which is the tool publishers use to manage their ad inventory. AdX, which is the exchange where buyers and sellers meet in milliseconds. And Google Ads and DV360, which are the tools advertisers use to buy. Owning all three layers meant Google could see what everyone was bidding before the auction settled, jump in to win at the last second, and systematically disadvantage any exchange or tool that competed with their own products.

The two most documented examples are Project Bernanke and Last Look. Project Bernanke used data from Google's buy-side tools to help AdX win auctions it otherwise would have lost. Last Look let AdX see the winning bid from header bidding competitors and beat it by a penny. Both ran for years before anyone outside Google knew about them. The court found this substantially harmed publishers who were leaving money on the table every single day without knowing it.

So the DOJ has two options now. The scalpel or the sledgehammer.

The scalpel means behavioral rules: force Google to make GAM work equally with competing exchanges, ban Last Look, open-source the auction logic, share data with competitors. The sledgehammer means selling AdX entirely, making it an independent company that has to compete on its own merits without Google's advertiser demand propping it up.

Both are legitimate remedies for what Google did. Here is my honest take though. The scalpel without real enforcement teeth is basically nothing. The DOJ argued this explicitly. They cannot be trusted to self-regulate. The sledgehammer seems to be the right call but runs into the problem of who actually buys AdX. Any large tech company that could afford it would trigger its own antitrust review. A private equity firm would be running critical internet infrastructure with no strategic interest in the health of the open web.

There is also an angle nobody is talking about enough. Let me put some actual numbers on it.

Google’s Network revenue, everything flowing through GAM and AdX on third party publisher sites, came in at roughly $31 billion in 2024. These are not broken out separately in Alphabet’s financials but AdX’s confirmed take rate is the key lever. The DOJ’s own expert witness testified it sits 19 to 27 percent above what a competitive market would support. Force that rate down to match Magnite or PubMatic at 10 to 15 percent and Network revenue falls to $15 to $18 billion, and that is before accounting for volume loss as advertiser demand shifts to other exchanges.

That sounds catastrophic until you look at the full picture. Alphabet crossed $400 billion in total revenue in 2025. A $15 billion hit to the Network business is less than 4 percent of total revenue. And the Network segment is already the only part of Google not growing, while Search, YouTube, and Cloud are all expanding at double digits.

So yes, GAM and AdX remain profitable under the scalpel. They do not go to zero. But here is the point that actually matters. At $15 to $18 billion with compressed margins and zero strategic data flowing back into the rest of Google's stack, this becomes a business Google has almost no incentive to maintain, invest in, or subsidize for small publishers anymore. The whole point of owning the ad stack was never the margins on AdX. It was the data. Every bid, every impression, every publisher signal flowing through GAM fed back into making Search and YouTube ads more valuable than anyone else's. Strip that data connection and you have a basic exchange charging basic fees.

With that said, even if the DOJ gets everything it wants, it does not fix what is actually killing publishers. Because the threat to the open web is not the Google tax. It is the zero-click future that chatbots are building right now.

THE REAL PROBLEM IS NOT IN THE COURTROOM

Here is what is actually happening while everyone is watching the antitrust trial. Google's AI Overviews, ChatGPT, Gemini, Claude and Perplexity are answering questions that used to require a click. Health information, travel planning, how-to guides, product comparisons, local recommendations. All of it is being summarized by AI before a user ever lands on a publisher's page. Penske Media, which owns Variety, Deadline, and The Hollywood Reporter, sued Google in September 2025 saying that AI Overviews were appearing on roughly 20 percent of searches linking to their sites, and that affiliate revenue from shopping links was down more than a third from the end of 2024 because of the traffic drop.

That is not a Google ad tech problem. Fixing AdX does not fix that. Banning Last Look does not fix that. The DOJ remedy, whatever it ends up being, addresses a market structure problem from the 2010s while the actual economic collapse of the open web is happening in 2026 from a completely different direction.

The New York Times and the Wall Street Journal did not move to subscriptions because they wanted to. They did it because the math stopped working. If you stay free and your content is publicly accessible, AI companies will scrape your journalism, summarize it, serve it to billions of users, and you get nothing. Not a click, not an ad impression, not a subscriber. Nothing. The paywall is not a business strategy. It is the only rational response to a world where your content has value to AI companies and zero value reaches you. Sure, there is GEO (Generative Engine Optimization) but it’s still in its infancy and publisher content will still be summarized with a link at the bottom that you could click if you want to. You probably won’t.

THE LICENSING DEALS ARE THE NEW BUSINESS MODEL AND MOST PUBLISHERS ARE NOT IN IT

Some publishers figured out how to get paid. The problem is which publishers.

News Corp signed a five-year deal with OpenAI reportedly worth more than $250 million, giving OpenAI access to the Wall Street Journal, Barron's, MarketWatch, The Times UK, and a dozen other properties. The Financial Times got a deal reportedly worth $5 to $10 million a year. The Guardian signed with OpenAI. The Washington Post signed with OpenAI. Reddit, which is not even a traditional publisher but happens to be the most cited source in AI models at three times the rate of Wikipedia according to Profound AI, got deals with both Google and OpenAI. Condé Nast, The Atlantic, Hearst, Axel Springer, the Associated Press. The list of publishers with deals reads like a who's who of the biggest media brands in the world.

That is the point. The deals are going to the publishers who have leverage. The ones with large audiences, recognizable brands, premium content, or unique data that AI companies genuinely need. Everyone else is getting harvested for free. The local news site, the independent blog, the niche trade publication, they are providing the content that trains the models that replace the need to visit them, and they are getting nothing in return.

The licensing model as it exists right now is not a sustainable framework for the open web. It is a private arrangement between the richest publishers and the richest AI companies. It is hush money at scale. News Corp CEO Robert Thomson called the OpenAI deal "the beginning of a beautiful friendship." What he did not say is that the friendship requires having enough leverage to get in the room in the first place.

WHERE THE MODEL NEEDS TO GO

Going back to what actually needs to happen, there are two paths being tried right now and neither one is complete.

The first is the licensing deal model. Pay publishers a flat fee for access to their content for training and retrieval. This is what most of the deals above are structured around. The problem is the evolution from flat rate to usage-based is just starting. People Inc., which did deals with both OpenAI and Microsoft, put it clearly on an earnings call. The Microsoft deal is pay-per-use and the OpenAI deal is all you can eat. Both can work as long as the content is respected and paid for. Reddit is pushing further, negotiating for dynamic pricing where they get paid more as their data proves more valuable to model outputs. That is the right direction.

The second model is the Prorata approach. More than 500 publishers have signed with Prorata, which runs an AI search engine called Gist.ai and gives publishers a 50 percent revenue share model based on how much their content actually gets used in generating answers. That is closer to what a fair system looks like. You get paid proportionally to your contribution. The problem is it only works within Prorata's ecosystem and it requires the major AI players like OpenAI and Google to adopt a similar framework, which they have very little incentive to do while the current arrangement lets them access most content for free.

The end state that actually sustains the open web is a standardized pay-per-response model where any AI company that uses a publisher's content to generate an answer owes that publisher a fraction of the value created. Not a one-time training fee. Not a flat annual license. A royalty tied to actual usage. This is what the music industry built with streaming after a decade of getting destroyed by piracy. Spotify pays per play. It is not a perfect system and artists argue constantly that the per-play rate is too low. But the model exists. Publishers and AI do not have that model yet and until they do, most of the open web is operating on borrowed time.

WHAT HAPPENS TO THE OPEN WEB

What you end up with is a bifurcated web and it is already taking shape.

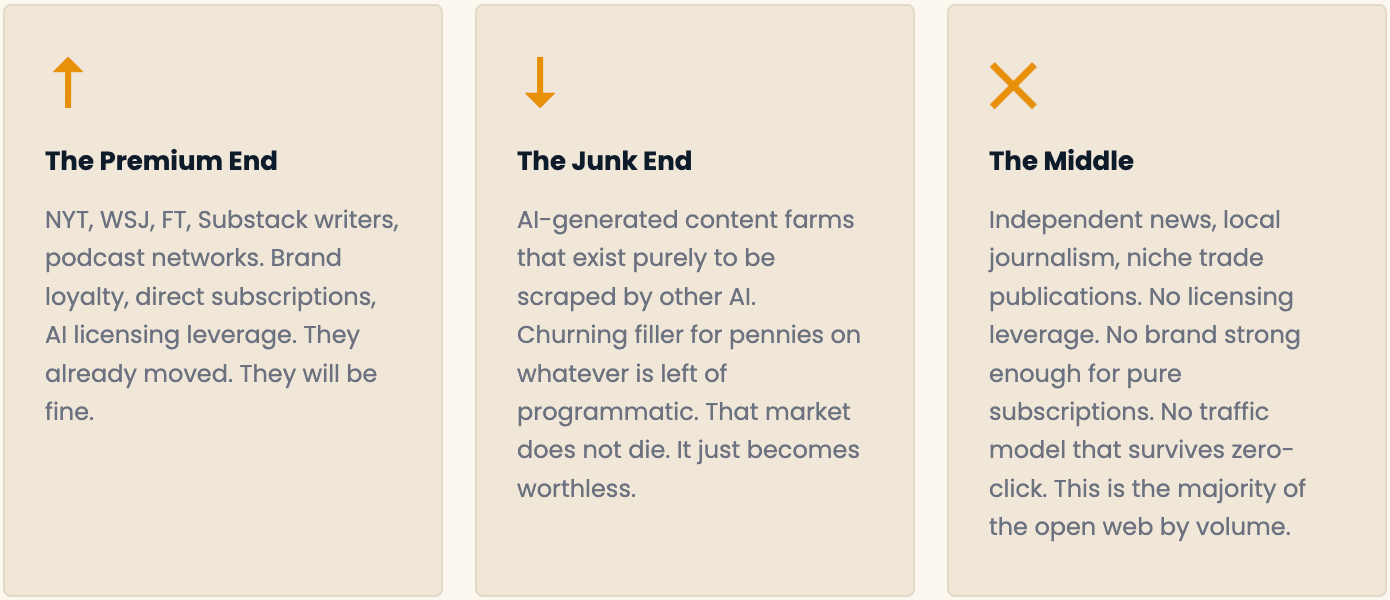

The premium end survives. NYT, WSJ, FT, The Atlantic, The Economist. Enough brand loyalty for direct subscriptions, enough leverage for AI licensing deals. They will be fine and they already moved. Substack writers, YouTube channels, and podcast networks also survive because they built direct audience relationships that do not depend on search traffic. AI Overviews do not threaten a newsletter your readers already subscribe to.

Then there is the junk end. AI-generated content farms that exist purely to be scraped by other AI, churning out filler that makes pennies through whatever is left of the programmatic ecosystem. That market does not die, it just becomes worthless.

The ones getting wiped out are in the middle. Independent news sites, local journalism, niche trade publications, specialty blogs. These are the publishers with no leverage in licensing negotiations, no brand strong enough to drive pure subscription revenue, and no traffic model that survives the zero-click era. This is the majority of the open web by volume. These are the ones the DOJ case was supposed to help. And these are the ones the DOJ case does not actually help.

The irony of the whole thing is that Google's argument throughout the antitrust case has been that their ad tech is what keeps the open web alive. And in a narrow, technical sense they were right. GAM and AdX did bring advertiser demand to publishers who had no other way to monetize. But the open web that Google claimed to be protecting was already being dismantled by a different Google product, AI Overviews, at the same time the lawyers were arguing in court. They were handing out lifejackets while quietly draining the pool. The right hand was subsidizing what the left hand was destroying.

WHAT I ACTUALLY THINK HAPPENS

The DOJ remedy, whatever form it takes, will matter for the ad tech industry. It will change the competitive dynamics between exchanges, give publishers better yield on the inventory they do sell, and remove the most outrageous forms of self preference that Google used to tilt auctions. That is worth doing.

But if you are a mid-size publisher watching your search traffic decline and your ad revenue compress at the same time, the AdX divestiture does not change your trajectory. You are in a race to either build a direct audience relationship, get into one of the AI licensing arrangements, or figure out something entirely different before the economics collapse entirely.

The real ruling that will matter for the open web is not Judge Brinkema's decision on AdX. It is whatever framework, legal or commercial, eventually determines how AI companies pay for the content they use to generate answers. The licensing deals happening right now are private, inconsistent, and tilted toward whoever has the most leverage. That is not a sustainable model and it is not a fair one.

We shall see how fast the industry gets there. But the DOJ case, for all its significance, is not the answer to that question.

It’s just a tax Google is willing to pay because it’s already won.